A SIAM Environment Series-Part 1

The first lecture of the two-part environment series provided an overview of the supplier and the OEM function, regulations and policy, and the economic impact of recycling ELVs.

Story by: Deepti Thore

Courtesy CERO (Mahindra MSTC Recycling Pvt. Ltd.)

Tackling End of Life Vehicles (ELVs) in an environmentally sensitive manner is at the core of safely reintroducing waste to new production. The sound management acts to transform waste into nutrients fed to the new product. This approach popularly known as the ‘cradle-to-cradle’ although not new to the automotive industry has room for immense headway. In India, a well-oiled recycling ecosystem is the crying need of the hour. The first lecture of the two-part environment series outlined such nitty-gritty. It provided an overview of the supplier and the Original Equipment Manufacturer (OEM) function, regulations and policy, and the economic impact of recycling ELVs. Setting the tone of the proceedings, exclaimed Rahul Mishra, Principal at Kearney, “The steady shift towards ELVs in India has multiple implications for all the stakeholders in the automotive industry in particular and the economy at large.”

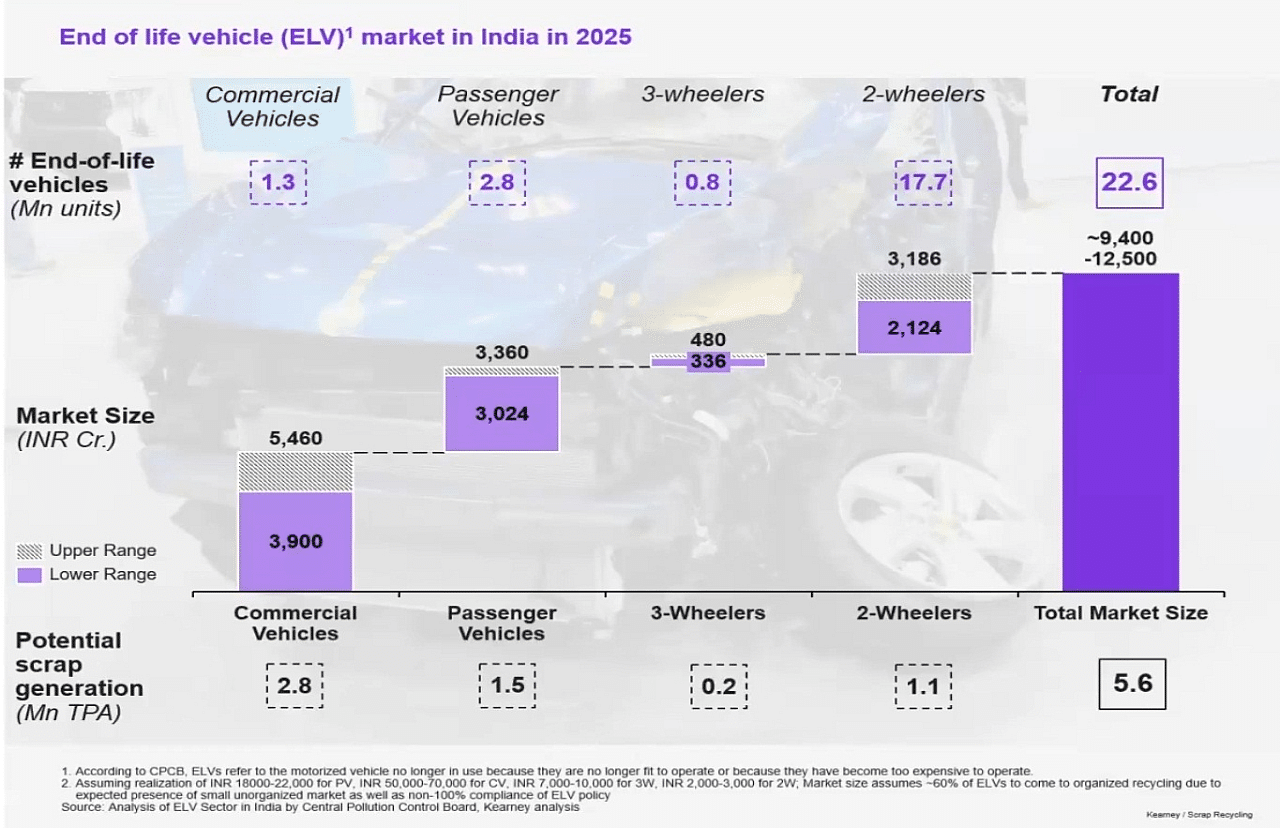

By 2025, ELVs in India is expected to reach a market size of 20-22 million at an estimated valuation of Rs.9400-12,500 crore, as per the Kearney study cited. In a further bifurcation, Shovik Banerjee, Principal at Kearney opined that the scrap generation from ELVs would touch a valuation of USD 5.6 million, by 2025. Projecting the contribution of different vehicular segments to ELVs over the next half a decade, Banerjee stated, passenger vehicles alone would be the second-largest contributor to ELVs at 10-30 per cent in a total passenger vehicle population (parc) of 12 per cent. Two-wheelers would make up for a 25-35 per cent share in a vehicle parc of about 80 per cent. Commercial vehicles would contribute the bulk of the share at 40-50 in a vehicle parc of six per cent, he pointed further.

Rahul Mishra, Principal, Kearney

Shovik Banerjee, Principal, Kearney

Key OEM and supplier considerations

With the scrappage policy announcement around the corner, OEMs and suppliers will be required to work closely and not in silos. On policy supporting the stakeholders, Shovik Banerjee, Principal at Kearney was quick to point at inefficiencies of the draft scrappage policy. “Scrap value chain is based on three key elements: collection and aggregation, dismantling and processing and sales and consumption. There is a need for putting in place other structural policies to support the transition,” he opined. Adding to it, Captain NS Mohan Ram, VSM, I.N (retired), FNAE, stressed on the risk factors involved around such a modernisation scale. “Shredding could be a viable option for India in the next three to four years. The need of the hour is to plan ahead for inclusions like post shredder treatment for the likely generation scale of Automotive Shredder Residue (ASR),” he explained. Notably, there are six major auto collection hubs in India with Delhi NCR region holding a 35 per cent share of contribution to recycling ELVs, as reported by Kearney. Guidelines issued by the Delhi government comply with the Central Pollution Control Board (CPCB) guidelines and provide a license to operate from Delhi. It provides a minimum 1000 sq.yard of non-residential area, CCTV cameras for surveillance, procedures for junk vehicles and covers diesel vehicles over 10 years and petrol vehicles over 15 years.

Courtesy CERO (Mahindra MSTC Recycling Pvt. Ltd.)

Masaru Akaishi, Managing Director, Maruti Suzuki Toyotsu India (MTSI)

Masaru Akaishi, Managing Director, Maruti Suzuki Toyotsu India (MTSI) drew attention to challenges anticipated for recycling ELVs including the ELV generation, collection, pre-treatments and safe dismantling all in a manner that the extracted low-value material is made useful for the future. Explained Akaishi, that ELV consists of a variety of materials oscillating between high-value aluminium and copper to low-value byproducts where the risk of dismantling or dumping low-value material is always high. In terms of environment-friendly ELV pre-treatment process, Akaishi stressed on the importance of setting aside waste oil and gasoline, freon gas and airbags ahead of the dismantling process even if it translated to an additional cost being incurred. Proper pre-treatment is mandatory for environment protection, he exclaimed. Akaishi called for the need to formulate a policy to ensure timely vehicle disposal or replacement, through a cut-off year on the lines of global best practices. For instance, Japan has two annual checking systems and China is known to restrict the issuing of new number plates. China, Europe and Japan also have a robust framework for lithium battery recycling. They also have a strong framework to educate the EV owners, he added. MSTI has begun work on its first plant in Noida, expected to be commissioned in early 2021.

Scrap-based steel production

Courtesy Toyota Tsusho India Pvt. Ltd.

Sanjay Mehta, President of Material Recycling Association of India apprised steel producers of ELVs being a game-changer for the industry. With ferrous scrap known to be the primary raw input for steel production, the government has been working closely with steel producers to establish metal scrapping centres in India. It is quintessential to ensure the scientific processing and recycling of ferrous scrap, likely to be generated from various sources. As per the government steel scrap recycling policy, scrap-based steel-making tech is key to reduce greenhouse gas emissions intensity. Steel manufacturers must adopt the principles of reduce, reuse, recycle, recover, redesign and remanufacture, he said. As per a study one-tonne of scrap has the potential to help the industry save 1.1-tonne of iron ore, 630 kg of coking coal and an estimated 55 kg of limestone. Energy consumption savings could be to the tune of 11 MJ/Kg (EAF/IF) which translates to an up to 17 per cent energy savings. To give a perspective, the global demand for steel scrap, a 2017 study, peggs the contribution of scrap at 475 million tonnes in the global steel production volume of 1688 million tonnes.

Among key drivers is the Ministry of Road Transport and Highways (MoRTh) guideline focussed on ELV recycling, details for licensing Authorised Vehicle Scrapping Facility (AVSF), deregistration or documentation process. It covers inspection, approval and renewal of the license. AIS 129, on the other hand, covers not only ELVs, but it also deals with the design and builds of new vehicles. The three-part recyclability includes collection and dismantling of ELVs, heavy metal restriction and type approval for Reusability, Recyclability and Recoverability (RRR). It follows EC regulations and also covers two-wheelers.

Kaushik Madhavan, Vice President – Mobility at Frost & Sullivan

The EV ecosystem

Drawing attention to the need for Shared Stakeholder Responsibility (SSR) between the battery and vehicle manufacturer, Kaushik Madhavan, Vice President – Mobility at Frost & Sullivan pointed out that advanced SSR is prevalent in China and the UK. In the UK, Kaushik mentioned, producers take back waste industrial batteries free of cost from the end-user. Awareness is generated to educate the end-users on the return process. Implementation of a shared responsibility framework where battery manufacturers invest in recycling or partner with authorised recycling facility, the nodal agency to monitor usage, OEMs to create end-user awareness and certification of logistics players involved with Hazmat transportation is also crucial. Taking China as a base case for his study, Kaushik urged EV manufacturers to consider setting up recycling channels and service outlets besides also setting up ‘traceability’ systems. The latter is deemed to be crucial for a successful value chain. The first of the two-part lecture series also urged the policy-makers to consider subsidies, incentives, resource allocation, and the formulation of an apex body for the speedy resolution of concerns to help in decision making. Encouraging investments from OEMs and battery manufacturers in second life applications was acknowledged as a key driver of successful ELVs recycling.

Energy storage demand

Citing the global trends in recycling and reusability of next-generation batteries, Madhavan urged the industry to benchmark its standard operating procedures of recycling and reusability for India with the global best practices. “The ecosystem that we set out to build must establish a circular economic value chain for the batteries,” he emphasised. Madhavan drew attention to the consolidated demand for lithium-ion battery-based energy storage that is known to kick in the second phase of the battery lifecycle. According to Madhavan, the industry must brace itself to cater to an estimated 8400 GWh storage capacity demand by 2027 possible through environmentally sound management of ELVs. ACI

Leave a Reply