MAIT with its knowledge partner Avanteum Advisors LLP draws attention to the critical role played by PCBA in the electronics value chain. Ashish Bhatia cites the emphasis in the study on building an ecosystem with enablers crucial to drive India’s global ambitions.

AIT together with its knowledge partner Avanteum Advisors LLP published a report to chalk out the roadmap to India’s leadership in the Printed Circuit Board Assembly (PCBA) industry. Well aware of the electronics segment being favoured globally for investment and growth, the report is quick to draw attention to the inherent opportunities across domains like materials, design, manufacturing and service besides the inherent potential of a multi-industry impact. With the National Policy on Electronics (NPE) 2019 pegging the industry valuation at USD 400 billion, the report expects it to be a crucial contributor to India’s 2025 goal of turning into a USD five trillion economy.

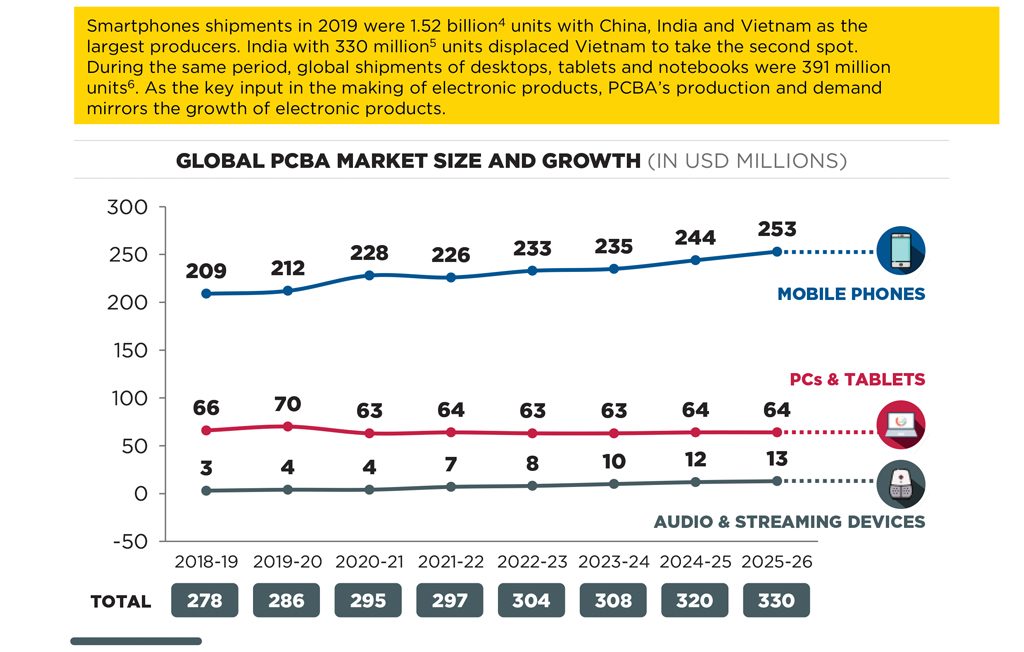

To live up to its potential, there is a need to build a potent ecosystem. One that facilitates a design-led manufacturing industry! A critical component in the value chain, PCBA, is said to contribute between 40-60 per cent of the product Bill of Materials (BoM). Notably, the growth of electronics in the Asian market is claimed to have been marked by the growth in PCBA manufacturing. China’s emergence as an electronics powerhouse defined by migration of global PCBA manufacturing led by EMS companies is the testimony, as per the study. The global PCBA demand expected to grow to USD 330 billion by 2025-26, driven by smartphones and computing devices. Here China, with a well-oiled ecosystem operating at a global scale, caters to nearly half of the global PCBA demand.

Over the last two decades, the migration of electronics manufacturing to Asia is said to have been the hallmark of the industry evolution. Malaysia, Thailand and Vietnam are among other countries to have witnessed a rapid growth in PCBA production. With companies de-risking with a China+1 strategy amidst the trade volatilities of the past year, India is expected to be deemed as a favourable destination. Global investors are deciding on basis scores of low-cost manufacturing and ease of doing business in countries like India. The domestic PCBA market in India, as a result, is expected to touch a valuation of USD 815 billion by 2025-26. Between 2020-21 and 2025-26, export revenues alone are expected to amount to USD 101 billion. Such projections make it all the more important to ensure a robust ecosystem is put in place. For it to be realised, PCBA manufacturing in the country is estimated to require a cumulative capital inflow of USD 25-30 billion by 2024-25.

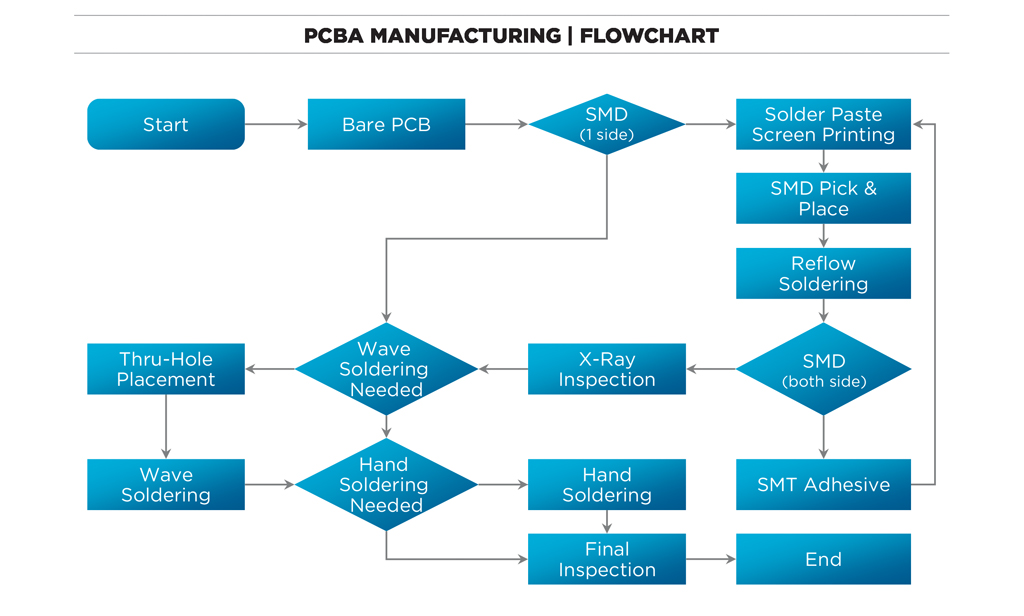

PCBA manufacture

Led by consumers seeking a better quality of life, the scale of electronics production has shown an upward trajectory. With higher economies of scale being realised, prices have seen a downward trend thus increasing affordability. In 2019, revenues were pegged at USD 2.9 trillion. Known to carry all the critical components required for an electronic product, the report pegs its value at the highest in EboM. Dependent on the type of electronic components, type of circuit board, and the end-use application of the board, the PCB used for assembly is segmented by layers, the density of interconnections, flexibility and IC substrate. As per Avanteum Analysis, based on the material type, PCBA and the PCBA market is segmented into FR-4, PFTE (Teflon) and metal.

Based on two manufacturing technologies: Thru-Hole Technology (THT) and Surface Mount Technology (SMT) differ in terms of process technology, application, advantages and disadvantages. The study claims, globally THT is less favoured due to the relative miniaturisation drive and cost of manufacturing PCBA. It is still holding a market of its own owing to cost and relatively larger form factor of many components. In comparison, SMT is said to be the chosen process for PCBA manufacturers. The report states that there is a place for both in the case of modern PCBA manufacturing.

The concentration in Asia

Led by the decline in cost of data services, smart devices have permeated into under-addressed markets, states the study. PCBA’s production and demand mirror the growth of electronic products. Accounting for 90 per cent of the production, Asia has benefitted from the production moving away from the US and Europe. Here China commands a 48 per cent share courtesy presence of global EMS companies in the country like Foxconn, Pegatron, Wistron, Flex and homegrown players like BYD and USI credited for the latter’s export capacity.

It is credited to an efficient supply chain and manufacturing cost led courtesy a desirable scale said to be found in EMS operations. The supply chain needs to be such that it is both cost-competitive and insulated from disruption. On the exports front, the IP prowess of both Korea and Japan have helped them retain a sizeable exports share. India, in comparison, finds itself uniquely positioned among countries leading in both production and consumption. The migration of PCBA manufacturing into India over the next few years is expected to be driven by aspirations to reduce import dependence. Known to have received 24 investments in electronics projects, the need of the hour is to develop capabilities in components along with OEM partnership for access.

Design-led manufacture

Manufacturing in India has not kept pace with the demand. The report claims, growth of domestic manufacturing has been restricted to the assembly of the imported components and modules. To become a global hub for electronics manufacturing and exports, India must prioritise domestic value addition and reduce dependence on core components in line with the ‘Atma Nirbhar Bharat’ mission plan. The need of the hour is for an active intervention at the assembly stage. Such an augmentation will draw investments into active, passive and mechanical components. It is also expected to help develop a component base and help attain the end objective of design-led manufacturing. The report adds that the design zone currently dominated by global captive centres will expand to include independent companies engaged in PCBA design to cater to both domestic and export needs.

The approvals received under the Production Linked Incentive (PLI) scheme is also expected to lead to capacity addition. With global companies known to be on the approved list, the prospects of creating a global manufacturing and supply centre in India have gone up too. That the top six global EMS players have a presence in India, and they have OEM partnerships promises assures committed operations. Notably, 14 players from the global top 20 players with combined revenue of USD 44 billion are yet to set up manufacturing in India. In line with the global trend, OEMs will continue to depend on EMS players for the benefits on offer.

The challenges

Despite the existence of Government schemes like PLI, SPECS and EMS 2.0, amidst the intense global competition, the local OEMs face multiple challenges. Domestic OEMs are dependent on imports to meet the demand for active, passive and mechanical components. Manufacturers are challenged by the lower demand volumes for individual components leading to uneconomical procurement. PCBA manufacturers suffer a price disadvantage of 20 per cent in the case of a six to eight-layer PCB procurement. This renders them incapable of procuring large volumes. The critical semiconductor Ics known to have origins in other countries is also depriving India of a direct source to forge partnerships.

Among cost-disabilities are China and Vietnam patronising their electronics industry and Corporate Income Tax (CIT) for new investments in the country at 15 per cent as per the World Bank EoDB report of 2020. To meet the USD 101 billion exports target, there is a need for a robust export strategy that overcomes the inconsistent incentive schemes. There is a need for a greater emphasis on localisation and assured preferential market access to encouraging domestic PCBA manufacturing. The government must allay the apprehensions of PCBA manufacturers through policy intervention and prioritisation of processing components bound for PCBA manufacturing. Plug and play manufacturing and access to a qualified talent pool is a must too. The report calls for treating new and existing investments at par about the PLI benefit extended. After all existing PCBA units are expected to deliver faster than the new entrants in the domain. ACI

———————————————

Known to work in multiple areas of public advocacy, including cloud and analytics, IPR, skill development, component hub, state IT/ESDM policies, import and export policy on one end of the spectrum and Innovation and startup, Industry 4.0 on the other end, MAIT’s key objective is to encourage domestic manufacturing through local innovation and IP creation. Focused on ensuring compliance of standards and regulatory framework favourable for nation-building, it is also involved in advocacy for a policy known to lead the development of the electronic hardware sector in India.

———————————————

Avanteum Advisors LLP is an advisory firm providing services on strategy, implementation and insights to organisations in the automotive, transportation, logistics and industrial segments.

Leave a Reply